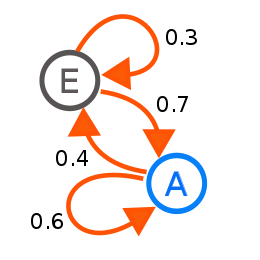

A diagram representing a two-state Markov process. The numbers are the probability of changing from one state to another state.

Part of a series on statistics

Probability theory

Probability

Axioms

Determinism

System

Indeterminism

Randomness

Probability space

Sample space

Event

Collectively exhaustive events

Elementary event

Mutual exclusivity

Outcome

Singleton

Experiment

Bernoulli trial

Probability distribution

Bernoulli distribution

Binomial distribution

Exponential distribution

Normal distribution

Pareto distribution

Poisson distribution

Probability measure

Random variable

Bernoulli process

Continuous or discrete

Expected value

Variance

Markov chain

Observed value

Random walk

Stochastic process

Complementary event

Joint probability

Marginal probability

Conditional probability

Independence

Conditional independence

Law of total probability

Law of large numbers

Bayes' theorem

Boole's inequality

Venn diagram

Tree diagram

v

t

e

A Markov chain or Markov process is a stochastic model describing a sequence of possible events in which the probability of each event depends only on the state attained in the previous event.[1][2][3][4] Informally, this may be thought of as, "What happens next depends only on the state of affairs now." A countably infinite sequence, in which the chain moves state at discrete time steps, gives a discrete-time Markov chain (DTMC). A continuous-time process is called a continuous-time Markov chain (CTMC). It is named after the Russian mathematician Andrey Markov.

Markov chains have many applications as statistical models of real-world processes,[2][5][6][7] such as studying cruise control systems in motor vehicles, queues or lines of customers arriving at an airport, currency exchange rates and animal population dynamics.[8]

Markov processes are the basis for general stochastic simulation methods known as Markov chain Monte Carlo, which are used for simulating sampling from complex probability distributions, and have found application in Bayesian statistics, thermodynamics, statistical mechanics, physics, chemistry, economics, finance, signal processing, information theory and speech processing.[8][9][10]

The adjectives Markovian and Markov are used to describe something that is related to a Markov process.[2][11][12]

^Richard Serfozo (24 January 2009). Basics of Applied Stochastic Processes. Springer Science & Business Media. p. 2. ISBN 978-3-540-89332-5. Archived from the original on 23 March 2017.

^ abcGagniuc, Paul A. (2017). Markov Chains: From Theory to Implementation and Experimentation. USA, NJ: John Wiley & Sons. pp. 1–235. ISBN 978-1-119-38755-8.

^"Markov chain | Definition of Markov chain in US English by Oxford Dictionaries". Oxford Dictionaries. Archived from the original on December 15, 2017. Retrieved 2017-12-14.

^Definition at Brilliant.org "Brilliant Math and Science Wiki". Retrieved on 12 May 2019

^Samuel Karlin; Howard E. Taylor (2 December 2012). A First Course in Stochastic Processes. Academic Press. p. 47. ISBN 978-0-08-057041-9. Archived from the original on 23 March 2017.

^Bruce Hajek (12 March 2015). Random Processes for Engineers. Cambridge University Press. ISBN 978-1-316-24124-0. Archived from the original on 23 March 2017.

^G. Latouche; V. Ramaswami (1 January 1999). Introduction to Matrix Analytic Methods in Stochastic Modeling. SIAM. pp. 4–. ISBN 978-0-89871-425-8. Archived from the original on 23 March 2017.

^ abSean Meyn; Richard L. Tweedie (2 April 2009). Markov Chains and Stochastic Stability. Cambridge University Press. p. 3. ISBN 978-0-521-73182-9. Archived from the original on 23 March 2017.

^Reuven Y. Rubinstein; Dirk P. Kroese (20 September 2011). Simulation and the Monte Carlo Method. John Wiley & Sons. p. 225. ISBN 978-1-118-21052-9. Archived from the original on 23 March 2017.

^Dani Gamerman; Hedibert F. Lopes (10 May 2006). Markov Chain Monte Carlo: Stochastic Simulation for Bayesian Inference, Second Edition. CRC Press. ISBN 978-1-58488-587-0. Archived from the original on 23 March 2017.

^"Markovian". Oxford English Dictionary (Online ed.). Oxford University Press. (Subscription or participating institution membership required.)

^Model-Based Signal Processing. John Wiley & Sons. 27 October 2005. ISBN 9780471732662.

A Markovchain or Markov process is a stochastic model describing a sequence of possible events in which the probability of each event depends only on...

In statistics, Markovchain Monte Carlo (MCMC) is a class of algorithms used to draw samples from a probability distribution. Given a probability distribution...

A hidden Markov model (HMM) is a Markov model in which the observations are dependent on a latent (or "hidden") Markov process (referred to as X {\displaystyle...

In the mathematical theory of probability, an absorbing Markovchain is a Markovchain in which every state can reach an absorbing state. An absorbing...

examples of Markovchains and Markov processes in action. All examples are in the countable state space. For an overview of Markovchains in general state...

In mathematics, the quantum Markovchain is a reformulation of the ideas of a classical Markovchain, replacing the classical definitions of probability...

distribution of a previous state. An example use of a Markovchain is Markovchain Monte Carlo, which uses the Markov property to prove that a particular method...

of MDPs comes from the Russian mathematician Andrey Markov as they are an extension of Markovchains. At each time step, the process is in some state s...

stochastic process satisfying the Markov property is known as a Markovchain. A stochastic process has the Markov property if the conditional probability...

known as the Markovchain. He was also a strong, close to master-level chess player. Markov and his younger brother Vladimir Andreevich Markov (1871–1897)...

stochastic matrix is a square matrix used to describe the transitions of a Markovchain. Each of its entries is a nonnegative real number representing a probability...

characterize continuous-time Markov processes. In particular, they describe how the probability of a continuous-time Markov process in a certain state changes...

scientists. Markov processes and Markovchains are named after Andrey Markov who studied Markovchains in the early 20th century. Markov was interested...

counting measures. The Markovchain is ergodic, so the shift example from above is a special case of the criterion. Markovchains with recurring communicating...

In the mathematical theory of random processes, the Markovchain central limit theorem has a conclusion somewhat similar in form to that of the classic...

balance in kinetics seem to be clear. A Markov process is called a reversible Markov process or reversible Markovchain if it satisfies the detailed balance...

) {\displaystyle O(a+b)} in the general one-dimensional random walk Markovchain. Some of the results mentioned above can be derived from properties of...

computationally intensive statistical methods including resampling methods, Markovchain Monte Carlo methods, local regression, kernel density estimation, artificial...

boundary were coined by Judea Pearl in 1988. A Markov blanket can be constituted by a set of Markovchains. A Markov blanket of a random variable Y {\displaystyle...

However, with the advent of powerful computers and new algorithms like Markovchain Monte Carlo, Bayesian methods have seen increasing use within statistics...

Global Information

Global Information