Implied volatility patterns that arise in pricing financial options

Volatility smile

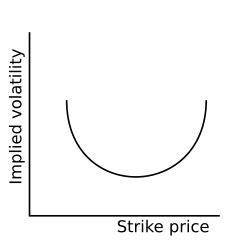

Volatility smiles are implied volatility patterns that arise in pricing financial options. It is a parameter (implied volatility) that is needed to be modified for the Black–Scholes formula to fit market prices. In particular for a given expiration, options whose strike price differs substantially from the underlying asset's price command higher prices (and thus implied volatilities) than what is suggested by standard option pricing models. These options are said to be either deep in-the-money or out-of-the-money.

Graphing implied volatilities against strike prices for a given expiry produces a skewed "smile" instead of the expected flat surface. The pattern differs across various markets. Equity options traded in American markets did not show a volatility smile before the Crash of 1987 but began showing one afterwards.[1] It is believed that investor reassessments of the probabilities of fat-tail have led to higher prices for out-of-the-money options. This anomaly implies deficiencies in the standard Black–Scholes option pricing model which assumes constant volatility and log-normal distributions of underlying asset returns. Empirical asset returns distributions, however, tend to exhibit fat-tails (kurtosis) and skew. Modelling the volatility smile is an active area of research in quantitative finance, and better pricing models such as the stochastic volatility model partially address this issue.

A related concept is that of term structure of volatility, which describes how (implied) volatility differs for related options with different maturities. An implied volatility surface is a 3-D plot that plots volatility smile and term structure of volatility in a consolidated three-dimensional surface for all options on a given underlying asset.

^Hull, John C. (2003). Options, Futures and Other Derivatives (5th ed.). Prentice-Hall. p. 335. ISBN 0-13-046592-5.

Volatilitysmiles are implied volatility patterns that arise in pricing financial options. It is a parameter (implied volatility) that is needed to be...

mathematical finance, the SABR model is a stochastic volatility model, which attempts to capture the volatilitysmile in derivatives markets. The name stands for...

A local volatility model, in mathematical finance and financial engineering, is an option pricing model that treats volatility as a function of both the...

long-observed features of the implied volatility surface such as volatilitysmile and skew, which indicate that implied volatility does tend to vary with respect...

interest-rate models, and the Derman–Kani local volatility or implied tree model, a model consistent with the volatilitysmile. Derman, who first came to the U.S....

In financial mathematics, the implied volatility (IV) of an option contract is that value of the volatility of the underlying instrument which, when input...

consistent with mixture models, applying this to volatilitysmile modeling in the context of local volatility models. He is also one of the main authors in...

volatilitysmile problem, one can drop the assumption that the volatility ( σ {\displaystyle \sigma } ) is constant. If we assume that the volatility...

implied volatility and market downturns. Yan (2011) presents an explanation for the equity premium puzzle using the slope of the implied volatilitysmile. The...

Volatility risk is the risk of an adverse change of price, due to changes in the volatility of a factor affecting that price. It usually applies to derivative...

In finance, volatility arbitrage (or vol arb) is a term for financial arbitrage techniques directly dependent and based on volatility. A common type of...

§ Portfolio theory above. Closely related is the volatilitysmile, where, as above, implied volatility – the volatility corresponding to the BSM price – is observed...

Calibration errors. Volatility is the most important input in risk management models and pricing models. Uncertainty on volatility leads to model risk...

establishing the so-called Dupire's approach to local volatility for modeling the volatilitysmile. The Dupire equation is a partial differential equation...

implied volatility. Another aspect that some speculators may find interesting is that the quoted strike is determined by the implied volatilitysmile in the...

to improve the horizontal radiation pattern Volatility skew, in finance, a downward-sloping volatilitysmile SKEW, the ticker symbol for the CBOE Skew Index...

Implied volatility, Volatilitysmile Local volatility Stochastic volatility Constant elasticity of variance model Heston model Stochastic volatility jump...

moneyness; this is useful in constructing an implied volatility surface, or more simply plotting a volatilitysmile. This section outlines moneyness measures from...

Laplace distribution) to address problems of skewness, kurtosis and the volatilitysmile that often occur when using a normal distribution for pricing these...

is correct. This method is therefore inappropriate when there is a volatilitysmile. For a more general but similar approach that uses numerical methods...

underlying swap. Adjustments may then be made for moneyness; see Volatilitysmile § Implied volatility surface. To use the lattice based approach, the analyst...

financial derivatives valuation in presence of the volatilitysmile in the context of local volatility models. This defines our application. The mixture...

Global Information

Global Information